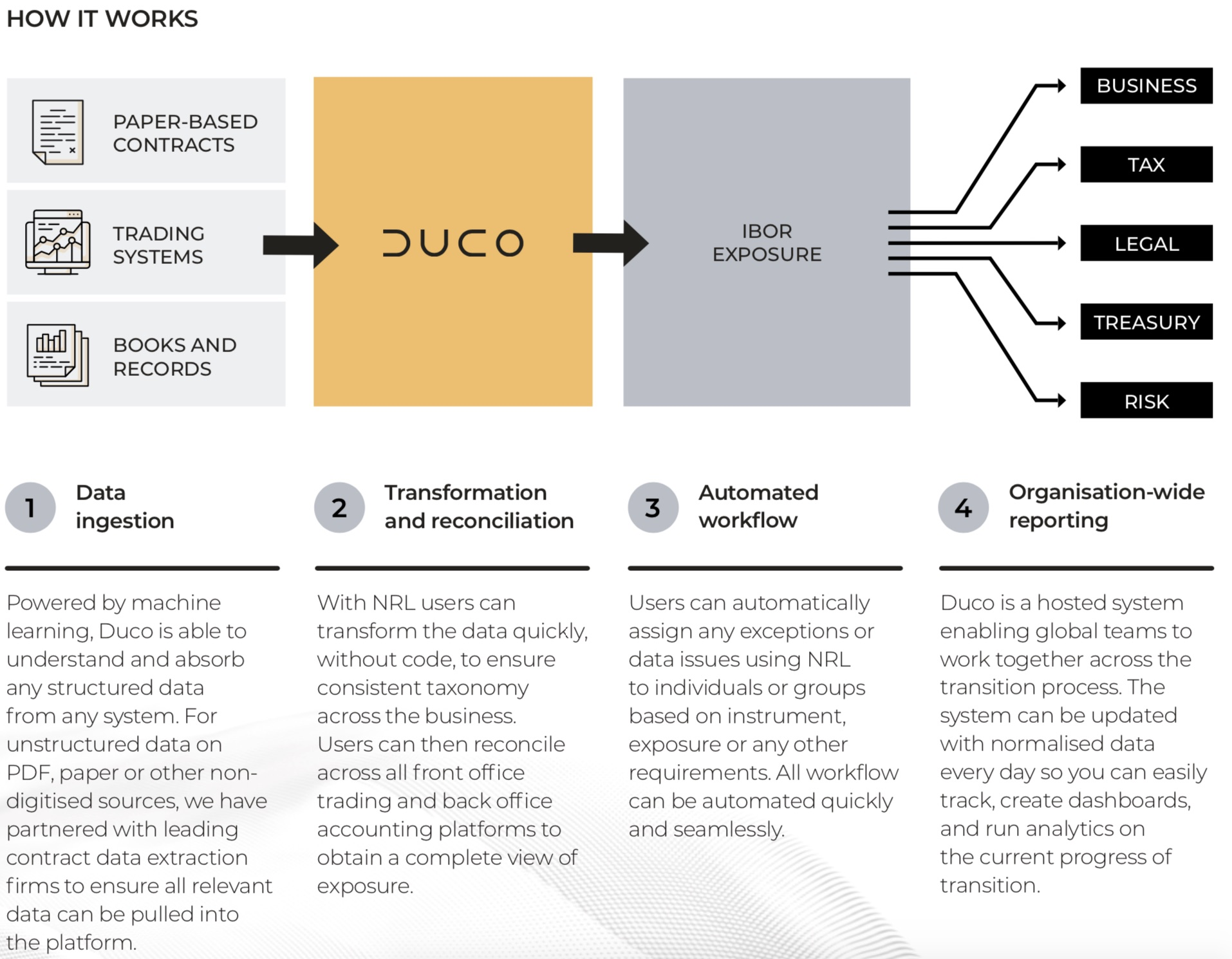

A COMPLEX DATA PROBLEM

Regulators globally have emphasised it is time for market participants to start transitioning from the use of Interbank Offered Rates (IBORs) in unsecured lending in favor of new alternative reference rates or ARRs. The transition will affect a wide range of departments within financial organisations, including tax, legal, treasury, operations and risk. To drive this change, consolidating data from these departments is critical to a successful transition. However, the data is vast and in many disparate systems, including risk platforms, front office trading, back office accounting, contract management systems or even printed files in a drawer. The data challenge is not just in the range of systems but the variety of data sets and contracts across the business.

THE NEED

A fully systematic approach is required to understand both contract and position exposure to IBOR across all asset classes with minimal human intervention. Firms need to be able to:

+ Ingest salient data from paper contracts into digital, readable forms

+ Reconcile all trading platforms across the organisation to obtain full exposure

+ Match digitised contracts with internal trading books to understand contract and position risk

+ Compare rates to understand risks during rebooking, and ensure complete rebooking of cancels/corrects

+ Provide centralised, automated workflow for all responsible teams

+ Dashboard and chart the analytics of all transition progress, outstanding issues and outstanding risk

THE DUCO DIFFERENCE

Duco offers a highly agile, rapidly deployed solution to handle the IBOR transition to ARRs. By using our next-generation technology, firms can ingest data from a range of digital and non-digital sources. From there, users can normalise and transform the data, without code, using our unique Natural Rule Language (NRL), extracting the necessary contract details and tying them out to the trading desk to start the transition. With Duco you can:

+ Ensure a unified view of position and contract exposure

+ Integrate meta and reference data to help automate the transition

+ Compare spread data of LIBOR to ARR to assist rebooking

+ Create filters for affected contracts (eg post December 2021 for GBP and USD)

+ Manage the entire transition process, all in one place